AI Trinity [Data * Design * Security]

Cost Method of Treasury Stock Accounting

January 26, 2024

Treasury Stock refers to a company’s own shares that it repurchases from the open market, thereby reducing the total number of outstanding shares available to investors. These repurchased shares don’t pay dividends, confer voting rights, or possess any ownership privileges. ABC Company has excess cash and believes its stock trades below its intrinsic value. As a result, it decides to repurchase 1,000 shares of its stock at $50 for a total value of $50,000.

How Treasury Stock Is Recorded

All such information is provided solely for convenience purposes only and all users thereof should be guided accordingly. Finance Strategists has an advertising relationship with some of the companies included on this website. We may earn a commission when you click on a link or make a purchase through the links on our site. All of our content is based on objective analysis, and the opinions are our own. No-par stock does not have a stated or par value per share, while par value stocks do. In effect, the balance of the Treasury Stock contra account is closed into the balance of the Common Stock account.

Get in Touch With a Financial Advisor

- Retired shares are treasury shares that have been repurchased by the issuer out of the company’s retained earnings and permanently canceled.

- An alternative method of accounting for treasury stock is the constructive retirement method, which is used under the assumption that repurchased stock will not be reissued in the future.

- For a long time, it was considered standard to include only the number of options and dilutive securities that are exercisable in the calculation of diluted shares, as opposed to outstanding.

- If the treasury stock is resold at a later date, offset the sale price against the treasury stock account, and credit any sales exceeding the repurchase cost to the additional paid-in capital account.

- When shares are repurchased, the treasury stock account is debited to decrease total shareholders’ equity.

- A company might purchase its own outstanding stock for a number of possible reasons.

Non-retired treasury shares can be reissued through stock dividends, employee compensation, or capital raising. Like treasury stock transactions, income or loss for the current period is not affected, nor can retained earnings be increased when capital stock is retired. the best tax software for us expats This loss does not affect the current period’s income but reduces the credit balance in the paid-in capital account that resulted from other treasury stock transactions. A company might purchase its own outstanding stock for a number of possible reasons.

Create a Free Account and Ask Any Financial Question

In this method, the company offers it shareholders a range within which they can bid to sell their shares. Finally, companies can also reacquire their shares by directly negotiating with their shareholders. These reasons may include blocking any takeover attempts that the company’s management or existing owners do not want to go through. Similarly, companies, that are publicly listed, and want to go private may also buy their shares back to decrease their number of shareholders. Sometimes, company management may choose to buy the shares of a company back when they have excess cash that they cannot find use for. Finally, some companies may have a policy of buying their shares back when the prices of the shares fall in the stock market.

What Is the Cost Method of Accounting for Treasury Stock?

These shares belong to the issuer even when they were initially issued at a discount rather than the market price. Treasury Stock simply refers to shares of company stock that have been repurchased by the issuing corporation. These are shares that have been bought back by the company either because it has no further use for them or because they think the stock is undervalued and represents a good investment. If the cost method is used, the entry is the same as for retirement except that the Treasury Stock account is credited instead of the Cash account. If a company has purchased treasury shares at a total cost of $25 per share, then sells those shares for $24, this transaction would cause an increase in Revenues and a decrease in Cash.

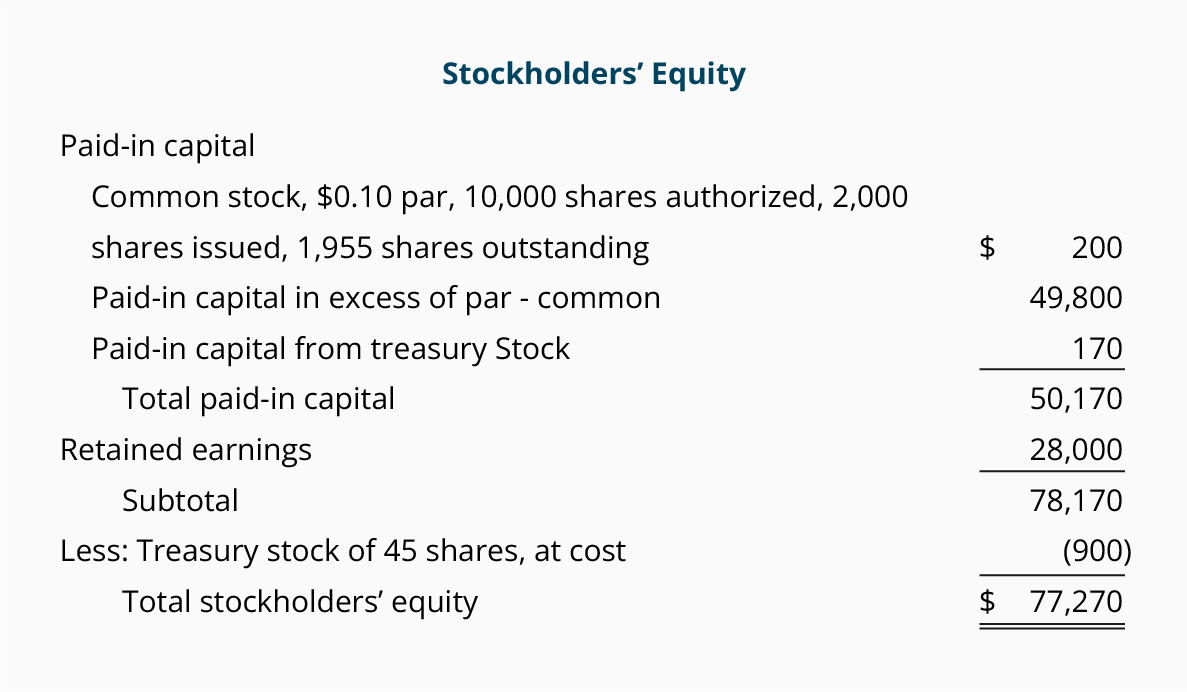

See also treasury stock and par value method (of treasury stock accounting). When a company purchases treasury stock, it is reflected on the balance sheet in a contra equity account. As a contra equity account, Treasury Stock has a debit balance, rather than the normal credit balances of other equity accounts.

If there is no balance in the Additional Paid-in Capital from Treasury Stock account, the entire debit will reduce retained earnings. When these shares are resold or reissued, the treasury stock is credited for the par value of these shares. Any additional receipts above the par value of the shares are taken to the additional paid-in capital account. However, this excess amount cannot be used to increase the retained earnings balance even if the reacquisition of the shares were set off against retained earnings. The issued shares are treated as if they are being issued for the first time with the treasury stock account being credited instead of the share capital account.

In the subsequent step, the TSM assumes the entirety of the proceeds from the exercising of those dilutive options goes towards repurchasing stock at the current market share price. The assumption here is that the company would repurchase its shares in the open market to reduce the net dilutive impact. Here, the number of shares repurchased is equal to the option proceeds (the number of gross “in-the-money” dilutive securities multiplied by the strike price) divided by the current share price. If treasury stock method is used, any purchase of treasury shares results in a credit to APIC and a debit to treasury stock at cost.

Once the shares of the company are issued, the company cannot regulate who owns their shares. However, some times, companies may choose to repurchase their shares from its shareholders. The company can choose to either retire these shares or resell them in the future. When shares are kept with the intention of future resale, these shares are known as treasury stock. On the shareholders’ equity section of the balance sheet, the “Treasury Stock” line item refers to shares that were issued in the past but were later repurchased by the company in a share buyback.

Its balance represents only the claims arising from the original investment of par value that were satisfied by distributing assets. If the cost is less than the original issue price, Additional Paid-In Capital should be credited. If the cost exceeds the original issue price, Additional Paid-In Capital or Retained Earnings should be debited. Callable stock (virtually always preferred shares) gives the corporation the right to buy the stock from the owner according to a prearranged schedule of prices and times.

Ranghan Venkatraman

CEO | CTO

Award Winning Entrepreneur, Member of the Forbes Technology Council, C-Suite advisor with unparalleled knowledge and experience in artificial intelligence, cloud, cybersecurity, and technology driven business model innovation.

"The world is powered by oxygen, water and now by algorithms"

Stay in the loop

Categories

Most Popular

- Cyber Rezilyens: Perils of Code Security (Injection)

Warning: Undefined variable $args in /var/www/html/wp-content/themes/rezilyens-child/single.php on line 151

Recent Posts

- Official site Pin Up 💰 Casino Welcome Bonus 💰 Betting & Casino Games

- Meilleur choix de casinos en ligne français

- Xslot Giriş: En İyi Online Casino Deneyimine Katılın

Warning: Undefined variable $args in /var/www/html/wp-content/themes/rezilyens-child/single.php on line 182